Curious about the pros and cons of 3-2-1 buydowns?

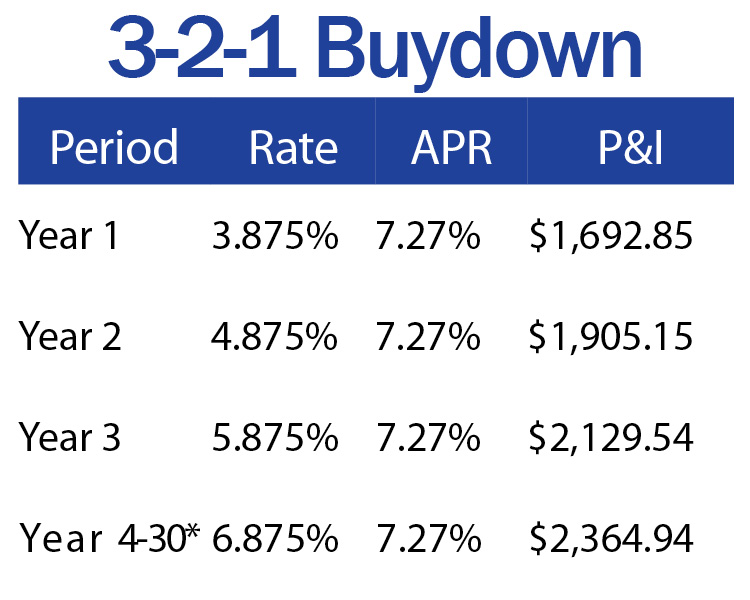

A 3-2-1 buydown is a mortgage assistance program that can help reduce your interest rate for the first three years of your loan. During the first year, your interest rate will be 3% lower than the standard rate, 2% lower in the second year, and 1% lower in the third year. After that, your interest rate will be the same as the standard rate for the remainder of your loan term.

There are several benefits to getting a 3-2-1 buydown. First, it can can save you money on your monthly mortgage payments, especially during the first three years of your loan. Second, it can help you qualify for a larger loan amount, since you will be able to afford a higher monthly payment. Third, it can give you peace of mind knowing that your interest rate will be lower for the first few years of your loan, which can help you budget more effectively.

There are also some potential drawbacks to getting a 3-2-1 buydown. First, it can increase the cost of your loan over time, since you will be paying a higher interest rate for the remaining years of your loan. Second, it can make it more difficult to refinance your loan in the future, since you will have to pay off the buydown amount before you can refinance.

Ultimately, whether or not a 3-2-1 buydown is right for you depends on your individual circumstances. If you are looking for a way to save money on your monthly mortgage payments and you are comfortable with the potential drawbacks, then a 3-2-1 buydown could be a good option for you.

3-2-1 buydown pros and cons

When considering a 3-2-1 buydown mortgage, it's important to understand both its potential benefits and drawbacks. Here are 8 key aspects to consider:

- Lower monthly payments: During the first three years of the loan, your monthly payments will be lower than they would be with a traditional mortgage.

- Qualify for a larger loan amount: With lower monthly payments, you may be able to qualify for a larger loan amount, allowing you to purchase a more expensive home.

- Budget more effectively: Knowing that your interest rate will be lower for the first few years can help you budget more effectively.

- Increased loan cost: Over the life of the loan, you will pay more in interest with a 3-2-1 buydown than you would with a traditional mortgage.

- Difficulty refinancing: It can be more difficult to refinance your loan in the future with a 3-2-1 buydown, since you will have to pay off the buydown amount first.

- Not always the best option: A 3-2-1 buydown may not be the best option for everyone. It's important to consider your individual circumstances and financial goals before making a decision.

- Can be combined with other programs: In some cases, a 3-2-1 buydown can be combined with other mortgage assistance programs, such as down payment assistance.

- May have tax implications: The tax implications of a 3-2-1 buydown can vary, so it's important to consult with a tax advisor to understand how it will impact your specific situation.

Ultimately, whether or not a 3-2-1 buydown is right for you depends on your individual circumstances and financial goals. It's important to weigh the pros and cons carefully before making a decision.

1. Lower monthly payments

This is one of the main benefits of a 3-2-1 buydown. With a traditional mortgage, your monthly payments will be the same for the entire life of the loan. However, with a 3-2-1 buydown, your monthly payments will be lower during the first three years of the loan. This can save you a significant amount of money, especially if you are on a tight budget.

For example, let's say you have a $200,000 mortgage with a 4% interest rate. With a traditional mortgage, your monthly payments would be $955. However, with a 3-2-1 buydown, your monthly payments would be as follows:

- Year 1: $812

- Year 2: $866

- Year 3: $920

Lower monthly payments can make it easier to afford a home, especially if you are on a tight budget. They can also free up cash flow for other expenses, such as saving for retirement or paying down debt.

2. Qualify for a larger loan amount

One of the main benefits of a 3-2-1 buydown is that it can help you qualify for a larger loan amount. This is because your monthly payments will be lower during the first three years of the loan, which means that you will have more money available to put towards your down payment and closing costs.

- Example: Let's say you have a $50,000 annual income and you are looking to buy a home. With a traditional mortgage, you may only be able to qualify for a loan amount of $200,000. However, with a 3-2-1 buydown, you may be able to qualify for a loan amount of $225,000. This is because your monthly payments would be lower during the first three years of the loan, which would free up more cash flow for your down payment and closing costs.

- Implication: Being able to qualify for a larger loan amount can give you more options when it comes to buying a home. You may be able to afford a larger home, a home in a more desirable neighborhood, or a home with more features. It can also give you more negotiating power when it comes to purchasing a home.

Overall, being able to qualify for a larger loan amount is a major benefit of a 3-2-1 buydown. It can give you more options when it comes to buying a home and it can help you get into a home that is a better fit for your needs.

3. Budget more effectively

One of the key benefits of a 3-2-1 buydown is that it can help you budget more effectively. With a 3-2-1 buydown, you will know exactly what your monthly mortgage payments will be for the first three years of the loan. This can give you peace of mind and help you plan your budget accordingly.

For example, let's say you have a $200,000 mortgage with a 4% interest rate. With a traditional mortgage, your monthly payments would be $955. However, with a 3-2-1 buydown, your monthly payments would be as follows:

- Year 1: $812

- Year 2: $866

- Year 3: $920

As you can see, your monthly payments would be significantly lower during the first three years of the loan. This could free up cash flow for other expenses, such as saving for retirement or paying down debt.

Knowing that your interest rate will be lower for the first few years can also help you make better financial decisions. For example, you may be able to afford to buy a more expensive home or you may be able to save more money for a down payment.

Overall, budgeting more effectively is a major benefit of a 3-2-1 buydown. It can give you peace of mind and help you plan your budget accordingly. It can also help you make better financial decisions and reach your financial goals faster.

4. Increased loan cost

It is important to understand that while a 3-2-1 buydown can save you money on your monthly mortgage payments during the first three years of the loan, you will ultimately pay more in interest over the life of the loan. This is because the interest rate on your loan will be higher during the last 27 years of the loan than it would be with a traditional mortgage.

For example, let's say you have a $200,000 mortgage with a 4% interest rate. With a traditional mortgage, you would pay $955 per month and a total of $229,920 in interest over the life of the loan. However, with a 3-2-1 buydown, you would pay $812 per month during the first year, $866 per month during the second year, and $920 per month during the third year. After that, your monthly payments would increase to $1,029 per month for the remaining 27 years of the loan. Over the life of the loan, you would pay a total of $244,440 in interest, which is $14,520 more than you would pay with a traditional mortgage.

The increased loan cost is an important factor to consider when deciding whether or not to get a 3-2-1 buydown. If you plan to stay in your home for the long term, you may end up paying more in interest over the life of the loan. However, if you plan to move within the first few years, a 3-2-1 buydown could save you money.

5. Difficulty refinancing

Refinancing a mortgage can be a great way to lower your monthly payments or interest rate. However, it can be more difficult to refinance your loan if you have a 3-2-1 buydown. This is because you will have to pay off the buydown amount first, which can add thousands of dollars to the cost of refinancing.

- Facet 1: Increased cost

The buydown amount is the amount of money that the lender pays to lower your interest rate during the first three years of the loan. This amount is typically added to the principal balance of the loan, which means that you will have to pay it back over the life of the loan. If you refinance your loan, you will have to pay off the buydown amount before you can get a new loan.

- Facet 2: Prepayment penalty

Some lenders charge a prepayment penalty if you refinance your loan within a certain period of time. This penalty can be several thousand dollars, which can make it even more expensive to refinance your loan.

- Facet 3: Impact on credit score

Refinancing your loan can have a negative impact on your credit score. This is because refinancing requires a hard credit inquiry, which can lower your score by a few points. If you have a low credit score, it may be more difficult to qualify for a new loan or you may get a higher interest rate.

Overall, it is important to consider the potential costs and benefits of refinancing your loan if you have a 3-2-1 buydown. In some cases, it may be possible to refinance your loan without paying off the buydown amount. However, it is important to talk to your lender to get a clear understanding of the costs and benefits involved.

6. Not always the best option

A 3-2-1 buydown can be a great way to save money on your monthly mortgage payments, but it's important to remember that it may not be the best option for everyone. Before you decide whether or not to get a 3-2-1 buydown, it's important to consider your individual circumstances and financial goals.

Here are a few things to consider:

- Your financial situation: A 3-2-1 buydown can be a good option if you have a low income or if you are struggling to qualify for a traditional mortgage. However, if you have a high income and you are able to qualify for a traditional mortgage, you may not need a 3-2-1 buydown.

- Your long-term goals: If you plan to stay in your home for the long term, a 3-2-1 buydown may not be the best option. This is because you will end up paying more in interest over the life of the loan. However, if you plan to move within the first few years, a 3-2-1 buydown could save you money.

- Your risk tolerance: A 3-2-1 buydown can be a risky option if you are not sure if you will be able to make your mortgage payments in the future. This is because if you default on your loan, you could lose your home.

If you are considering a 3-2-1 buydown, it's important to talk to a lender to get more information and to make sure that it is the right option for you.

7. Can be combined with other programs

Combining a 3-2-1 buydown with other mortgage assistance programs can significantly improve its benefits and make homeownership more accessible to low- and moderate-income borrowers. By combining these programs, homebuyers can reduce their upfront costs, lower their monthly mortgage payments, and potentially qualify for a larger loan amount.

One common combination is a 3-2-1 buydown with down payment assistance. Down payment assistance programs provide financial assistance to homebuyers who cannot afford the full down payment on a home. This assistance can come in the form of grants, loans, or bonds. By combining a 3-2-1 buydown with down payment assistance, homebuyers can reduce their upfront costs and make it easier to qualify for a mortgage.

Another common combination is a 3-2-1 buydown with closing cost assistance. Closing costs are the fees and expenses associated with getting a mortgage, such as the appraisal fee, loan origination fee, and title insurance. Closing cost assistance programs provide financial assistance to homebuyers who cannot afford to pay these costs upfront. By combining a 3-2-1 buydown with closing cost assistance, homebuyers can reduce their upfront costs and make it easier to purchase a home.

Combining a 3-2-1 buydown with other mortgage assistance programs can make homeownership more affordable and accessible to a wider range of homebuyers. If you are considering a 3-2-1 buydown, be sure to ask your lender about other programs that you may be eligible for.

8. May have tax implications

A 3-2-1 buydown can have tax implications, both positive and negative. It's important to understand these implications before you decide whether or not to get a 3-2-1 buydown.

- Facet 1: Mortgage interest deduction

One of the potential tax benefits of a 3-2-1 buydown is that it can increase your mortgage interest deduction. The mortgage interest deduction allows you to deduct the interest you pay on your mortgage from your taxable income. This can save you a significant amount of money on your taxes, especially if you have a high mortgage balance.

- Facet 2: Private mortgage insurance (PMI)

If you have a down payment of less than 20%, you will likely have to pay private mortgage insurance (PMI). PMI is an insurance policy that protects the lender in the event that you default on your loan. PMI can be expensive, and it can increase your monthly mortgage payments. However, a 3-2-1 buydown can help you avoid PMI by reducing your loan-to-value (LTV) ratio. This is the ratio of your loan amount to the value of your home.

- Facet 3: Capital gains tax

When you sell your home, you may have to pay capital gains tax on the profit you make. The profit is the difference between the sale price of your home and your cost basis. Your cost basis is the amount you paid for your home, plus any improvements you have made. A 3-2-1 buydown can reduce your capital gains tax by reducing the cost basis of your home. This is because the buydown amount is added to your loan balance, which increases your cost basis.

- Facet 4: State and local taxes

The tax implications of a 3-2-1 buydown can also vary depending on your state and local laws. Some states and localities have special rules for 3-2-1 buydowns. For example, some states do not allow you to deduct the buydown amount from your taxable income. It's important to check with your state and local tax authorities to find out how a 3-2-1 buydown will affect your taxes.

Overall, the tax implications of a 3-2-1 buydown can be complex. It's important to consult with a tax advisor to understand how a 3-2-1 buydown will impact your specific situation.

FAQs about 3-2-1 Buydown Pros and Cons

This section addresses common questions and misconceptions regarding 3-2-1 buydown mortgage programs, providing clear and informative answers to assist readers in making informed decisions.

Question 1: What is the primary advantage of a 3-2-1 buydown?

Answer: The main benefit of a 3-2-1 buydown is the potential for significant savings on monthly mortgage payments during the first three years of the loan term. This reduction in payments can provide financial relief and make homeownership more affordable for many individuals and families.

Question 2: Are there any drawbacks to a 3-2-1 buydown?

Answer: While a 3-2-1 buydown can offer initial savings, it's important to note that the interest rate on the loan will be higher during the remaining term of the mortgage. This means that the overall cost of the loan may be greater compared to a traditional mortgage with a fixed interest rate.

Question 3: Is a 3-2-1 buydown suitable for everyone?

Answer: The suitability of a 3-2-1 buydown depends on individual circumstances and financial goals. It may be a good option for those seeking lower monthly payments in the short term, particularly if they anticipate moving or refinancing within the first few years. However, if long-term savings and stability are prioritized, a traditional mortgage with a fixed interest rate may be more appropriate.

Question 4: Can a 3-2-1 buydown be combined with other financial assistance programs?

Answer: Yes, in some cases, a 3-2-1 buydown can be combined with other mortgage assistance programs, such as down payment assistance or closing cost assistance. This can further reduce the upfront costs of homeownership and make it more accessible to a wider range of individuals.

Question 5: Are there tax implications associated with a 3-2-1 buydown?

Answer: The tax implications of a 3-2-1 buydown can vary depending on individual circumstances and local tax laws. It's advisable to consult with a tax professional to fully understand the potential tax consequences before making a decision.

In summary, a 3-2-1 buydown can be a valuable tool for reducing monthly mortgage payments in the short term. However, it's crucial to carefully consider the potential drawbacks and suitability based on individual financial goals and circumstances. Consulting with a mortgage professional and a tax advisor can provide valuable insights and ensure an informed decision.

Transition to the next article section: "Exploring Alternative Mortgage Options for Homebuyers."

Conclusion

In exploring the advantages and disadvantages of 3-2-1 buydown mortgage programs, it is evident that these financial instruments can provide both benefits and drawbacks for homeowners. While they offer the potential for lower monthly payments in the initial years of the loan term, it is crucial to consider the long-term implications, including the higher interest rates and potentially increased overall loan costs.

The decision of whether or not a 3-2-1 buydown is the right choice depends on individual circumstances and financial objectives. Homebuyers seeking immediate savings on monthly payments may find it advantageous, especially if they plan to move or refinance within the first few years. However, those prioritizing long-term stability and lower overall loan costs may be better suited with a traditional fixed-rate mortgage.

It is recommended to consult with mortgage professionals and tax advisors to gain a comprehensive understanding of the implications and suitability of a 3-2-1 buydown based on specific financial situations and goals. By carefully weighing the pros and cons, homeowners can make informed decisions that align with their long-term financial interests and homeownership aspirations.

You Might Also Like

The Ultimate Guide To Marc Utay's ExpertiseMeet Lloyd G Trotter: The Renowned Architect Who Shaped Skylines

How Much Is A 1910 Quarter Worth Today?

Forecast On CEI Price: Get Informed Before Investing

Meet David Pinsen: An Innovator In The Tech Industry

Article Recommendations

- The Ultimate Guide To 80s Fashion Unleash Your Inner Icon

- The Life And Family Of Niall Horan An Indepth Look At His Wife And Son

- Unveiling The Mystery Of Tom Burke Wife Everything You Need To Know